Die Analyse und Prognose der Konjunktur ist eine Kernkompetenz des WIFO und bildet seit der Gründung des Institutes 1927 eine Säule der wissenschaftlichen Tätigkeit.

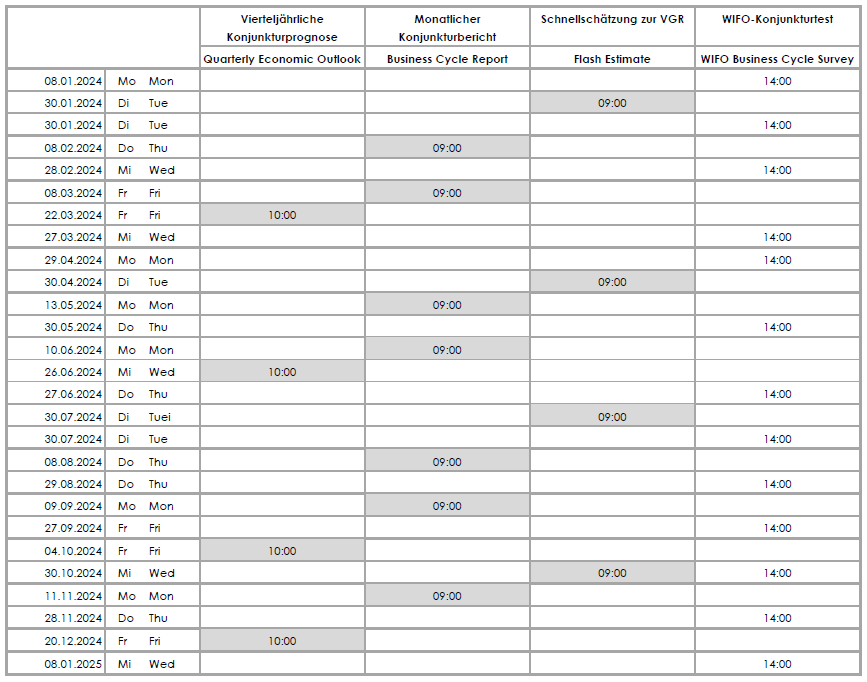

Im Rahmen seines Schwerpunktthemas "Konjunktur und Wachstum" legt das WIFO als zentrale Publikationsformate die vierteljährlichen Konjunkturprognosen und die laufenden Konjunkturberichte sowie die jährliche mittelfristige Prognose für Österreich und die Weltwirtschaft vor. Als Basis für die Konjunkturprognose dienen die Schnellschätzung des WIFO zur Volkswirtschaftlichen Gesamtrechnung VGR ("Flash Estimates") sowie die Ergebnisse des WIFO-Konjunkturtests (in Zusammenarbeit mit der Europäischen Kommission) und der anhand der Umfrageergebnisse und anderer (hochfrequenter) Konjunkturindikatoren erstellte Wöchentliche WIFO-Wirtschaftsindex.

Grundlage der kurz- und mittelfristigen Prognosetätigkeit sind ökonometrische Modelle, die auch zur Evaluierung wirtschaftspolitischer

Maßnahmen eingesetzt werden.